(This post originally appeared on the author’s blog.)

The government reported that the economy grew by 3.2% for the first quarter. Normally, that’s not so bad but for coming out of a deep recession, it’s very unimpressive.

Federal government spending, which includes remaining stimulus money, grew at an annualized rate of 1.4 percent in the first quarter of 2010. But this was more than offset by continued spending cuts from state and local governments, whose spending decreased 3.8 percent. It was the third quarter in a row in which state and local spending fell.

“Government spending contracted, for all the ballyhoo about stimulus,” said John Ryding, chief economist at RDQ Economics. “This recovery is going to have to stand on the backs of private-sector demand, not on government demand, given all the current fiscal challenges.” Even though any pickup in business is welcome, modest improvement may not be enough to alleviate the pain caused by the so-called Great Recession, many economists say.

The nation’s gross domestic product — a broad measure of goods and services produced in the country — is far below its potential, according to economists’ projections of where the economy would have been if it followed its long-term trend. Output would need to grow at least 5 percent annually for several years to get back on track — and perhaps more importantly, to lead to enough job creation to employ the 15 million Americans already out of work and the 100,000 new workers joining the labor force each month.

Earlier this week, I took a stab at giving a letter name to this recovery. My guess for Q1 was pretty close but a tad too high (I had 3.5% instead of 3.2%). Here’s the up-to-date chart:

Thanks to several emailers, I’m going to call it an N-Shaped recovery.

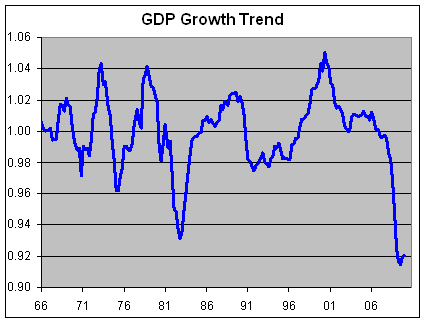

Here’s a more sobering way to look at GDP. This chart shows real GDP divided by a trendline growing at 3.08% which is about the long-term rate of growth.

In other words, this shows you how well GDP is doing compared with its historic growth rate. We’ve fallen off a cliff and are in the process of splatting.

In previous recessions, the economy has snapped back sharply to its historic trendline (1.0 on the chart). By growing at 3.2% last quarter, the economy is barely making headway.

At 0.92, we’re 8% below the trendline. This is what the NYT means by growing at 5% for a few years to get back on track. If the economy grew by 5% a year — 2% higher than the long-term trend — for four years, then we’d finally get back to something resembling normal.

Join the conversation about this story »

(This is a guest post from

(This is a guest post from