Rick Mills has put together a very good overview of the Lithium sector, production cycles and basic economics for Lithium Brines and Hard Rock Lithium mining. For us it is interesting to use his check lists to evaluate properties of International Lithium Corp. in Lithium Brines and Hard Rock Lithium. Mariana project in Argentina fits very well into described model for Lithium Brine Deposit. Company has put in a new presentation its own exploration models for Mariana Salar in Argentina and its Brine Lithium projects in Nevada.

Rick Mills has put together a very good overview of the Lithium sector, production cycles and basic economics for Lithium Brines and Hard Rock Lithium mining. For us it is interesting to use his check lists to evaluate properties of International Lithium Corp. in Lithium Brines and Hard Rock Lithium. Mariana project in Argentina fits very well into described model for Lithium Brine Deposit. Company has put in a new presentation its own exploration models for Mariana Salar in Argentina and its Brine Lithium projects in Nevada.

“

Company has posted new presentations for TNR Gold and International Lithium from PDAC in Toronto in March 2010. Interesting to note here is that REE Big Beaverhouse property is presented in TNR Gold portfolio – can we expect company activities to be centered around REE after lithium assets spin out?“TNR Gold Corp. is employing the project generator model. For those of you who may not know what a project generator model is, a word of explanation is in order. “Project generators” are companies that pick up early stage exploration ground when there are historical or scientific reasons to believe a property is prospective for a given mineral. Because these properties are obtained at an early stage of development, the cost of obtaining them is very low.As a project generator,TNR then uses its intellectual capital rather than hard currency capital to add value to its shareholders. By carrying out relatively low cost early exploration work, it demonstrates with greater confidence, the potential for a given property to host an economically viable mineral deposit. At that point in time, TNR hopes to bring in other companies that are willing and able to spend considerably more money to explore and advance those prospects toward production. TNR will generally retain a carried interest in those prospects into the future or at least a Net Smelter Return on any future production from the property. The prospect generator model is in theory a less risky model because, if other companies are spending considerable amounts of money, they can reduce the number of shares issued to raise capital.”

Lithium ABCs

Contributed by Rick Mills

As a general rule, the most successful man in life is the man who has the best information

The Puna plateau sits at an elevation of 4,000m, stretches for 1800 km along the Central Andes and attains a width of 350–400 km. The Puna covers a portion of Argentina, Chile and Bolivia and hosts an estimated 70 – 80% of global lithium brine reserves.

The evaporate mineral deposits on the plateau – which may contain potash, lithium and boron – are formed by intense evaporation under hot, dry and windy conditions in an endorheic basin – endorheic basins are closed drainage basins that retain water and allow no outflow – precipitation and inflow water from the surrounding mountains only leaves the system by evaporation and seepage. The surface of such a basin is typically occupied by a salt lake or salt pan. Most of these salt lakes – called salars – contain brines which are capable of providing more than one potentially economic product.

This Puna Plateau area of the Andean mountains – where the borders of Argentina, Bolivia and Chile meet and bounded by the Salar de Atacama, the Salar de Uyuni and the Salar de Hombre Muerto – is often referred to as the Lithium Triangle and the three countries mentioned are the Lithium ABC’s.

a Brine “Mining” Business Model

The salt rich brines are pumped from beneath the crust that’s on the salar and fed into a series of large, shallow ponds. Initial 200 to +1,000 parts per million (ppm) lithium brine solution is concentrated by solar evaporation and wind up to 6,000 ppm lithium after 18 – 24 months.

The extraction process is low cost/high margin and battery grade lithium carbonate can be extracted. The cost-effectiveness of brine operations forced even large producers in China and Russia to develop their own brine sources or buy most of their needed raw materials from brine producers.

The major lithium producers, from brine, are the “Lithium Three”: Sociedad Quimica y Minera (SQM), Rockwood/Chemetall and FMC.

The Lithium Three are all extracting lithium from Puna Plateau salar brines. The majority of lithium produced today comes from brines in Chile, Argentina and Nevada.

These brines are considered primarily potash deposits with lithium as a by-product.

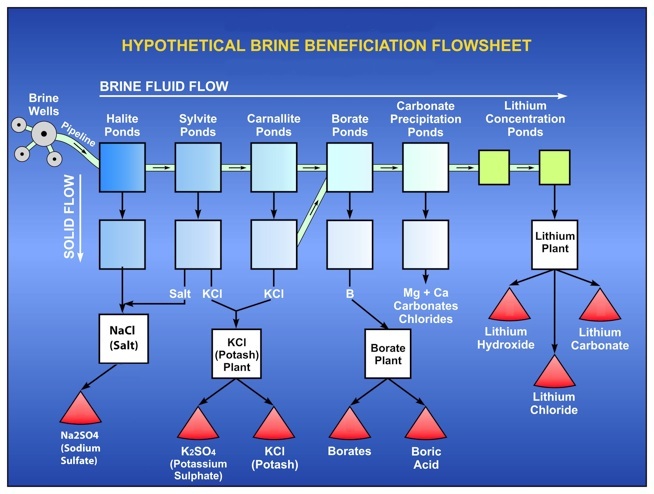

The above diagram was designed to show that several commercial products can be recovered from typical brine and that the recovery takes place in a series of steps over the entire evaporation process. Note that the final product in each step may require processing in a specialized plant. Also please note that the actual sequence of process steps may vary from brine to brine, and as such, the process steps shown above may not be in the correct order for any specific brine.

SQM’s Atacama brine deposits have the highest lithium content on the Puna – yet just 11% of its 2009 revenues were from lithium – 70% of SQM’s revenues are from fertilizers. SQM is the world’s largest producer of lithium and lithium is SQM’s highest gross margin product at +50%.

Potash is Fuel for Food

According to the United States Geological Survey (USGS) Canada has the world’s largest reserves of potash – roughly 50%. Coming in second is Russia with just over 25% and trailing a distant third is Belarus at 9% of world reserves.

In a presentation at the 2010 Prospectors and Developers Association Conference in Toronto Ontario, Canada, T.D. Newcrest minerals analyst Paul D’Amico forecast significant growth of offshore potash demand. D’Amico said the potash supply situation is complicated by the fact there hasn’t been a green field potash development in 30 years. D’Amico also estimated that global annual potash demand growth will average 3% compounded annually.

Potash is used as a major agricultural component in 150 countries but the largest importers of potash are China, India, the US and Brazil.

Potassium sulfate is commonly used in fertilizers, providing both potassium and sulfur. Potash is the common name for potassium chloride.

Because the financial markets crashed and the economy contracted in 2008 farmers put off buying potash – potash use fell 20%, phosphate fertilizer use declined 10% and the price per tonne of potash dropped by two thirds. This lack of fertilization drastically depleted the soil nutrient base and global soil nutrient levels need to come back to the trend line.

“Failure to feed the fields is a trend that can’t last for long, while the global recession severely impacted fertilizer demand, the science of food production has not changed. The significant volumes of potash and phosphate that have been mined for crop production must be replaced to sustain the productivity of the soil.” Potash Corp.

The basic fundamentals of the global potash market are hard to ignore:

• An increasing global population – the world’s population is steadily increasing and is expected to reach +9 billion people by 2050. The United Nations Food and Agriculture Organization (FAO) reported they think that the total world demand for agricultural products will be 60 percent higher in 2030 than it is today.

• Increasing incomes in developing countries will lead to more people being able to afford protein rich diets – a western style diet heavy in meat – which means more grain consumption.

• Decreasing arable land – arable land is being lost at the rate of about 40,000 square miles per year. Land is being used for production of bio-fuels, topsoil is eroded away by wind and water and the agriculture land base is being paved over as we become more and more urbanized. Farmers need to produce more food on less land. There is only one way this can be done and that’s with an increase in the use of fertilizer.

The current potash market is estimated at 50 million tonnes annually and is projected to grow at a compounded annual rate of 3-4%. Potash is a crucial element in fertilizer and has no commercial substitute. Quite simply, we have to grow more food on less land.

There are several ways farmers can get increased yields, Genetically Modified Organism (GMO) seed, pesticides, fertilizers, and satellite (GPS) farming.

Improved seeds, pesticides and new farming techniques are all going to be needed, improved and used. But the nutrients in soil are soon used up by ever more intensive farming – and Mother Nature can’t replace them fast enough. These nutrients need to be replaced or you have land where crops cannot grow.

Lithium

The world’s future energy course is being charted today because of the ramifications of peak oil and a need to reduce our carbon footprints.

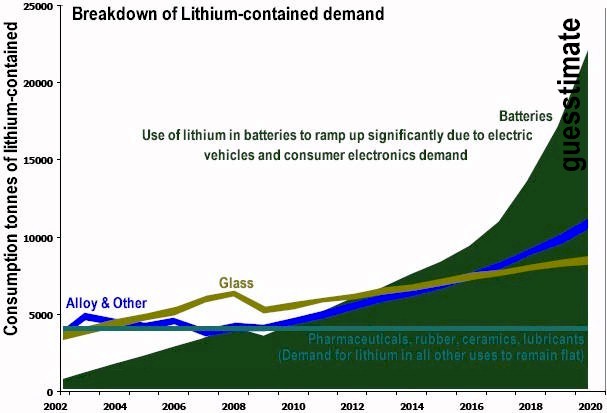

A whole new industry – a global wide automotive and industrial lithium-ion battery industry – is going to be built. As a result of lithium-ion battery demand for hybrid-electric and electric cars the increase in demand for lithium carbonate is expected to increase four-fold by 2017.

Lithium-ion batteries have become the rechargeable battery of choice in cell phones, computers, hybrid-electric cars and electric cars. Chrysler, Dodge, Ford, GM, Mercedes-Benz, Mitsubishi, Nissan, Saturn, Tesla and Toyota have all announced plans to build lithium-ion battery powered cars.

Demand for lithium powered vehicles is expected to increase fivefold by 2012. The worldwide market for lithium batteries is estimated at over $4 billion per year.

Lithium carbonate is also an important industrial chemical:

• It forms low-melting fluxes with silica and other materials

• Glasses derived from lithium carbonate are useful in ovenware

• Cement sets more rapidly when prepared with lithium carbonate, and is useful for tile adhesives

• When added to aluminum trifluoride, it forms LiF which gives a superior electrolyte for the processing of aluminum

• Lithium carbonate can be used in a type of carbon dioxide sensor.

Demand today is in the range of 120,000 tonnes of lithium carbonate equivalent (LCE) annually. Lithium is not traded publicly – and is usually distributed in a chemical form such as lithium carbonate (Li2CO3) – instead it’s sold directly to end users for a negotiated price per tonne of Lithium carbonate (Li2CO3).

Production figures are often quoted in lithium carbonate equivalent quantities. By weight approximately 18.8% of lithium carbonate is lithium. Therefore 1kg of lithium is the equivalent of 5.3 kg of lithium carbonate.

“We are projecting 40% Li demand increase by 2014, with batteries accounting for 34% of use, the largest single end-use segment.” Jon Hykawy, analyst Byron Capital Markets

Lithium-ion batteries are quickly becoming the most prevalent type of battery used in everything from laptops to cell phones to hybrid and fully electric cars to short term power storage devices for wind and solar generated power. At present, 39 per cent of lithium-ion batteries are produced in Japan, 39 per cent in China and 20 per cent in South Korea.

“With forecast 10% to 20% penetration rates by 2020 for pure and hybrid electric vehicles, we expect an incremental increase in demand of 286,000 tonnes of lithium carbonate equivalent, significantly outstripping current supply.” Canaccord Adams analyst, Eric Zaunscherb

“Our electric vehicle investment is not one-car innovation, it is a new way of looking at our industry. This is the beginning of the story.” Carlos Ghosn, Nissan chief executive officer

Sodium Chloride (rock salt or halite)

The principal use for salt is in the chemical manufacturing business – chloralkali and synthetic soda ash producers use salt as their primary raw material.

Salt is used in many applications and almost every industry:

• Cooking

• Manufacturing pulp and paper

• Setting dyes in textiles and fabric

• Producing soaps, detergents, and other bath products

• Major source of industrial chlorine and sodium hydroxide

Global demand for salt is forecast to grow 2.5 percent per year to 305 million metric tons in 2013.

Solar evaporation is the most popular and most economical method of producing salt. China is the world’s largest consumer of salt – other than the dietary needs of 1.3 billion people – there’s an enormous chemical manufacturing industry being built in China.

Boron

Boron combines with oxygen and other elements to form boric acid, or inorganic salts called borates.

Borates are used for:

• Insulation fiberglass

• Textile fiberglass

• Heat-resistant glass

• Detergents, soaps and personal care products

• Ceramic and enamel frits and glazes

• Ceramic tile bodies

• Agricultural micronutrients

• Wood treatments

• Polymer additives

• Pest control products

• Boron is an essential component in the manufacture of borosilicate glass used in LCD screens

Boric Acid uses:

• As an antiseptic/anti-bacterial compound

• Insecticide

• Flame retardant

• In nuclear power plants to control the fission rate of uranium*

• As a precursor of other chemical compounds

*Boric acid is used in nuclear power plants to slow down the rate at which fission occurs. Boron is also dissolved into the spent fuel cooling pools containing used fuel rods. Natural boron is 20% boron-10 which can absorb a lot of neutrons. When you add boric acid to the reactor coolant – or to the spent fuel rod cooling pools – the probability of fission is reduced.

The first half of 2009 saw a sharp drop in demand for borates, but in the second half of the year markets for both textile-grade fibreglass and borosilicate glass recovered.

World production of borates remains mostly concentrated in the US and Turkey – these two countries account for 75% of supply.

Chinese boron – both in terms of quantity and grade – is inadequate to meet domestic demand so the country is now the largest importer of both natural borates and boric acid.

Silly Putty was originally made by adding boric acid to silicone oil. J

Considerations – may I see junior’s grades?

The key factors that determine the quality, economics and attractiveness of brines are:

· Potassium content

· Lithium content

· Presence of contaminants ie magnesium (Mg)

· Porosity

· Net evaporation rate

· Recoverable by-products

· Infrastructure – or lack thereof

· Country risk

· 100% control over production

· Low capex, low production costs, high margin products

A common industry axiom says that the ratio of Mg to Li in brines must be below the range of 9:1 or 10:1 to be economical. This is because the Mg has to be removed by adding slaked lime to the brine – the slaked lime reacts with the magnesium salts and removes them from the water. If the ratio is 1:1 in the original brine, then the added cost (due to today’s present cost per tonne of slaked lime) is $180/tonne of lithium carbonate produced. If the Mg to Li is 4:1 than the cost of removing magnesium is $720.00 per tonne of lithium carbonate.

The porosity of a rock is expressed as a percentage and refers to that portion of the rock that is void space – rock that is composed of perfectly round and equal sized grains will have a porosity of 45%. Fluids and gases will be found in the void spaces within the rock.

Ten million cubic metres of brine bearing rock with a porosity of 10% will contain one million cubic metres of brine fluid. A cubic metre is equivalent to a kilolitre.

Salar de Atacama apparently has a porosity of about 8%. By oil and gas standards 8% is quite low, but brines are less viscous than hydrocarbon fluids and will flow more easily through rocks with lower porosity and permeability characteristics.

A major factor affecting capital costs is the net evaporation rate – this determines the area of the evaporation ponds necessary to increase the grade of the plant feed. These evaporation ponds can be a major capital cost. The Salar de Atacama has higher evaporation rates (3200 mm pan evaporation rate per year (py) and >

Contributing to efficient solar evaporation and concentration of the Puna Plateau brines are:

• Low rainfall

• Low humidity

• High winds

• High elevations

• Warm days

Though its evaporation rate is only about 72 percent of Atacama’s, Salar de Hombre Muerto is still commercially successful because costs are low and are further offset by the sale of recoverable byproducts like boric acid.

Rockwood Holdings recover moderate tonnages of potassium chloride as a co-product at their Chile operation. SQM recovers potassium chloride, potassium sulphate and boric acid.

According to FMC’s website they have:

• High concentrations of lithium – reportedly between 680 and 1210 ppm Li

• High in potassium – concentrations from 0.24 to 0.97 wt% K

Chile and Argentina supply 78% of global lithium carbonate and hold more than 90% of the proven lithium carbonate reserves.

The Salar de Uyuni (Bolivia) has the lowest average grade of Li at .028 and has an extremely high ratio of Mg/Li at 19.9

Uyuni’s higher rainfall and cooler climate means that its evaporation rate is not even half that of Atacama’s. The lithium in the Uyuni brine is not very concentrated and the deposits are spread across a vast area. Bolivia also has limited infrastructure – compared to that of Chile, Argentina or the US – and they lack free access to the sea.

Consider also the high “country risk” factor companies face doing business in Bolivia. Evo Morales, Bolivia’s President, has already nationalized the oil and gas industry – who’s next?

“The state doesn’t see ever losing sovereignty over the lithium. Whoever wants to invest in it should be assured that the state must have control of 60% of the earnings.” Morales at a March 2009 press conference

“The previous imperialist model of exploitation of our natural resources will never be repeated in Bolivia. Maybe there could be the possibility of foreigners accepted as minority partners, or better yet, as our clients. ” head of lithium extraction Saul Villegas

In 1990 hunger strikes and massive protests forced US based Lithco out of a $46 million investment into Bolivia’s Salar de Uyuni. The company set up operations at Argentina’s Salar de Hombre Muerto, and eventually became part of FMC.

It’s not surprising to this author that while Chile and Argentina have thriving lithium and potash production Bolivia lags far behind.

A company should have 100% control over the production rate from their salar. It’s possible an aquifer can become diluted – over producing can impact the brine’s salt concentrations and chemical compositions – or depleted by too many wells sucking up more brine than should be produced.

If two or more companies have straws (wells) into the same salar legal battles might result over the sharing of the resources.

“Lithium production via the brine method is much less expensive than mining. Lithium from minerals or ores costs about $4,200-4,500/tonne (€2,800-3,000/tonne) to produce, while brine-based lithium costs around $1,500-2,300/tonne to produce.” John McNulty, analyst Credit Suisse.

Global lithium production was dominated by the US – until the 1980s – with hard rock mining from spodumene. The better economics of the Chilean/Argentine salars priced hard rock lithium mining out of the markets.

There are exceptions – Talison Minerals has its Greenbushes operation (a combined tantalum and lithium mine) in Australia. This is the largest, highest grade lithium (spodumene) pegmatite deposit in the world and recent price increases have enabled them to sell their production to China for transformation into lithium carbonate. Two other producers of lithium ore concentrates are mostly concerned with the glass industry.

Hard rock lithium miners have two large problems facing them when competing with brine economics – firstly most have large capital (capex) costs for start up and secondly their production cost is roughly twice what it is for the brine exploitation process. These higher production costs are because of the different extraction processes used.

When lithium chloride reaches optimum concentration – using nothing more than sun and wind – the liquid is pumped to a recovery plant and treated with soda ash, precipitating lithium carbonate. The carbonate is then removed through filtration, dried and shipped.

In the case of production from pegmatites the process is:

· Mining

· Concentration to a higher grade

· Calcination at 1100 degrees Celsius to produce acid-leachable beta spodumene

· Treated with sulphuric acid at 250 degrees Celsius

· conversion of the lithium sulphate solution with sodium carbonate

This author believes investors will see development financings and start-up capital flow towards advancing the easier, quicker to production and cheaper to produce brine deposits rather than the higher start up cost and more expensive to produce hard rock mining situations.

There is room in the market for first mover juniors now positioned with quality salar packages in Argentina and Chile. Competition in these markets will not hurt margins for any company, old or new, due to the potential for exponential demand growth of potash and lithium.

But

The prime candidates have to be the lowest cost producers from both a capital (land package costs and capex) and variable (ie removal of contaminents) cost point-of-view.

(Rick Mills has put information about some junior mining companies with an important disclaimer, we did not verify information about those companies and do not know them apart from Orocobre story, please, visit the article with the link at the headline – S.)

Conclusion

“We think lithium-ion batteries for electric vehicles are the best technology.” Don Walker, CEO Magna International Inc.

“Magna wants to be on the leading edge of any new technology, and so we jumped on this technology a few years ago. The high-cost is the battery. So, working on the supply chain, getting the price down, and working on new composites for the battery are all things we are working on.” Ted Robertson, Magna’s chief technical officer

We seem to be going through an Eco-Energy Revolution – consider the ongoing nuclear renaissance, the surge towards energy retrofitting, cleaning up the environment and billions of dollars being given out to develop the technology behind the lithium-ion battery for the electrification of our transportation system.

This energy revolution is a serious investable long-term trend and we, as investors, have to take advantage of the opportunities being presented. We’d be smart to get in early, ahead of the herd, to take advantage of the coming global rush to electricity – generated by nuclear power and stored in lithium-ion batteries.

“The power of population is indefinitely greater than the power in the earth to produce subsistence for man”. Thomas Robert Malthus

The U.N. calls the global food crisis a “silent tsunami” and faith in the ability of local and global commodity markets to fill 6.6 billion bellies, never mind the projected 2.7 billion more by 2050 (U.N. projections say the world’s population will peak at 9.3 billion in 2050) has been shaken.

Are the words of Thomas Malthus coming back to haunt us?

In order for a plant to grow and thrive, it needs a number of different chemical elements. Three of these are the macronutrients nitrogen, phosphorus and potassium (a.k.a. potash, the scarcest of the three). Potassium makes up 1 percent to 2 percent of any plant by weight and is essential to metabolism. The availability of nitrogen, phosphorus and potassium in the soil, in a readily available form, is the biggest limiter to plant growth.

“Strong farmer returns, a depleted distributor pipeline and the agronomic need to replace soil nutrients have kick-started a potash rebound from 2009 lows.” Potash Corp. CEO Bill Doyle

Potash Corp – the world’s largest fertilizer maker – issued cautious guidance in January saying it expects first-quarter earnings to be between $1.30 and $1.50 per share which is well above its previous forecast of .70 – $1.00 per share.

“The upward revision reflects a sharp rebound in potash demand that is expected to drive a record quarter for North American sales volumes and strong offshore shipments,” the company said in explaining the revision.

This Brine “Mining” Business Model should be on every investors radar screen.

Is it on yours?

Richard (Rick) Mills”