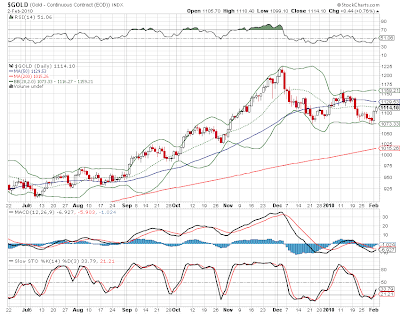

CS. Above is what we are calling

“Treasury Bubble”, it is weekly chart and it is still “safely” in a Bubble deflation mode. Everybody, who was “flying to safety” in the end of 2008 are sitting on huge by bond market definition losses. You can always hold it to maturity, but what will your money worth at that moment? We will make today just a few observations, regarding short term picture in USD, Gold and Juniors, highly leveraged to the first two factors.

We have mentioned before about

Gold Sell signal and suggested that there will be a time to accumulate Juniors, which will provide more upside opportunities with another Leg Up in the gold market. As it was scary before with gold over 1200 USD/oz, when everybody was bullish – so it is now very comforting to hear that Soros is suggesting that gold is a Bubble, Prechter is waiting for 40% correction and everybody is bearish about the Gold. Chart at the top does not give a lot of room for error like Google freedom of search exercise in China or weapons delivery to Taiwan. Henry Paulson shared in his book that Russians were talking Chinese into selling Agencies’ Debt (FNM and FRE) just before the crisis hit the world. Chinese apparently did not use the moment and “even provided support” for FED and US Treasury actions in the market during unfolding of economic crisis in 2008. They still have those “weapons of mass distraction” – billions of US IOU. And if we can agree that nobody, including Chinese, needs US Dollar Collapse overnight, we can not believe that U.S has the luxury to drive them mad with Taiwan and recent announcements about Obama meeting with Dalai Lama. Short term signals are difficult to read, but US Dollar chart above does not suggest a run away drive at the moment – recent US Dollar rally looks tired. Please, do not forget Obama’s success or what has left out of his rock-n-roll appearance depends on Jobs, not US Dollar chart. Recent budget suggested that even interest to pay on outstanding debt will be borrowed effectively, so it is basically a definition of insolvency. State can play the game longer then normal households, but now even Moody’s suggests that there are limits even to their AAA raiting to be stretched. Tim the Secretary was worried in front of Congress during the budget presentation about the same thing. His destiny was in the hands of Obama – literally: during his hug, before addressing the Nation. Question is: what can they really do with reappointed Mr Bernanke other than to print money to keep the Debt rolling?

Gold smells this uncertainty of proposed marriage of political will and fiscal discipline – when task is larger than life you can not just crunch the numbers, you have to be inventive and creative: TARP, Open window, Small business financing, Jobs Program – it is all about the money given to somebody. If you do not have them in the first instance you have to borrow or make more of it (before you borrow). Do you still follow us? We have lost it as well – we only know the big picture about which is the article below: the more creative fiscal and budget situation in the U.S. – the

less confidence will be left in US Dollar. Gold is trying to make a double bottom reversal on a short term basis on the chart above. Coupled with US Dollar rally coming out of steam, political determination to bring jobs at any cost and coming elections after lost Kennedy seat – correction could be over even before reaching long term support around 1000 USD/oz.

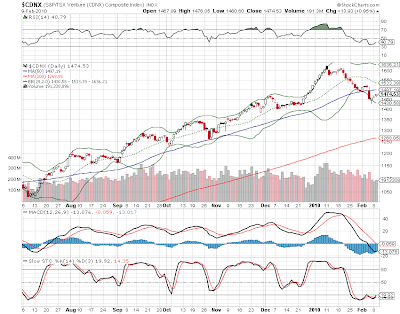

If all the above will prove to be correct in coming weeks, CDNX representing Canadian Juniors is making another high low at the MA50 support line and provides another buying opportunity into this Gold and Silver Bull. Do not discount our

Lithium and REE plays as well along the road –

inflation will bring excitement back with every dollar uptick in the Oil price above 75 USD/barrel. Once Sir Greenspan has suggested that Real Estate market is fragmented in nature and can not represent the Bubble (contrary to our modest observations and respectful disagreement at that time) – what if Tim and Ben will not be able to keep all those money on FED balance sheet and out of reach of their friends? After all, some of them were chosen and are still making the “God’s job”. Who can resist such a proposition?

The Independent suggests that it will be very difficult:

We are out of politics – our mind is too cynical in nature and instead baseless speculation we will provide more on gold fundamentals in the article below.

GATA:

Submitted by cpowell on Fri, 2010-01-29 20:46. Section:

Daily DispatchesRemarks by John Embry

Chief Investment Strategist

Sprott Asset Management, Toronto

Vancouver Resource Investment ConferenceHyatt Regency Hotel

Vancouver, British Columbia, Canada

Monday, January 18, 2010

Good afternoon. It is once again a great pleasure for me to address a knowledgeable gathering at Joe Martin’s always excellent Cambridge Conference.

When I was here last year gold was around $850 and there was the usual angst among mainstream commentators fearing a drop to $600 per ounce or worse. Today the price is roughly $300 higher and the same individuals continue to try to frighten the public with prophesies of vertiginous falls in the gold price. Despite this ongoing aggravation, I am even more bullish on the prospects for gold than I was a year ago.

However, despite my consistent enthusiasm for the yellow metal once termed a “barbarous relic” by Lord Keynes, I still have the strong feeling that the vast majority of investors outside this room still haven’t got a clue about gold and they are certainly not aware that gold is experiencing a historic bull market with much, much further to go. What we have seen to date is merely a prelude, and the appreciation we are going to see in future years is going to greatly exceed what we have seen to date. This opinion is based on a number of factors I will expand on, but the predominant theme is that gold is re-establishing itself as money.

It has been money for thousands of years, a reality that was succinctly summed up by J.P. Morgan in 1912 when he said, “Gold is money and nothing else.” But we go through periods when that reality is obscured, and the decades of the 80s and 90s represent living proof of that. Gold retreated to commodity status in that era, when disinflation was in vogue and the real returns on financial assets were truly remarkable in historic terms.

Gold fell from a peak of $850 per ounce in January 1980 to a low of $252 in July 1999 in an extended bear market. To be fair to gold, it got a significant push to the downside in the latter part of that period from the central banks that were dumping enormous quantities of gold by leasing it through their bullion bank cronies. I would contend that the gold price overshot its economic value by perhaps $150 on the downside. Contributing to this fiasco was the ludicrous auction of half the British gold reserves within 10 percent of the bottom. Today this egregious error is referred to as “the Brown bottom” in recognition of the idiocy of the current British prime minister, who was then finance minister.

However, this is all water under the bridge and I don’t particularly want to dwell on it other than to say that we are now in the phase of the gold market where we are about to benefit mightily from the central bankers’ awesome stupidity at that time.

It is important, though, that everyone realize exactly what happened. The Western central banks supplied massive quantities of gold to the market for at least the past 15 years. Initially this facilitated excessive producer hedging. Then it helped to fund a huge carry trade that greatly enriched their bullion bank cronies. Now it occurs in large part to protect existing huge short positions held by those same banks.

You might be inclined to ask why the central banks would do such a thing. The official explanation for the transparent portion of their activities (i.e., direct sales) was to diversify their reserves. Essentially, why hold gold when you can own an interest-bearing piece of paper in its stead?

But that explanation is purely fatuous and a total smokescreen. The whole process, with the clandestine leasing and swapping of huge quantities of gold, was orchestrated by the United States. It was designed to reduce critical scrutiny of the central banks’ increasingly reckless monetary policy, to allow interest rates to remain at unrealistically low levels and to maintain the U.S. dollar’s supremacy. That this undertaking would inevitably spawn serial financial bubbles, the very same bubbles that brought the world financial system to its knees, was conveniently ignored.

This was all foreshadowed by some remarkable comments by then-Federal Reserve Chairman Alan Greenspan at a Federal Open Market Committee meeting in the early 1990s, remarks that came to light only recently when a transcript of that meeting was scrutinized. Greenspan referred to gold as a “thermometer” and speculated that if the Treasury Department sold a little gold in the market and the price broke as a result, not only would the thermometer no longer be a measuring tool but the lower gold price could affect underlying psychology. Greenspan was unfortunately right in his perverse judgement and shortly thereafter the systematic dumping of gold by the Western central banks moved into high gear.

It really makes you love free markets, doesn’t it?

But what a sorry mess they have created. While in the ’90s, their gambit played out spectacularly with gold collapsing and financial assets flourishing, it sowed the seeds for what has happened subsequently: a robust bull market in gold since 2001 and increasing chaos in the stock, debt, and real estate markets worldwide. To this day the central bankers have remained undaunted and have increasingly intervened in all markets, but despite their annoying periodic raids, their influence is waning dramatically in the gold market.

I would suggest that today central banks are discovering to their increasing discomfort what history has always demonstrated — and that is that manipulation of the free-market process ultimately fails. No amount of government interference and price manipulation can change the reality of the free market over the long term.

In the whole sordid process of the gold suppression scheme for the past 15 years, what has been particularly intriguing to me is that an earlier generation of central bankers unsuccessfully tried to same ploy with gold in the 1960s. Using the considerably more transparent London Gold Pool, they succeeded in holding gold at the then-official price of $35 per ounce for a number of years before being overwhelmed by the reality of the situation. In the following decade of the 1970s, gold rose a mere 2,300 percent.

Armed with the knowledge of that fiasco, one would have surmised that our current central bank geniuses might have considered that their new attempts at price control, albeit considerably more secretive, could meet a similar fate. Alas, the hubris of central bankers is well known, and this just represents another graphic example of their arrogance and awesome incompetence.

However, what remains to play out is the denouement of their current folly. Markets that have been artificially capped tend to catapult upward when the suppression inevitably fails. In my opinion the last experience in the ’60s and ’70s was a mere bagatelle in comparison to what is unfolding today. It has always been accepted that “the greater and longer the manipulation, the greater the eventual price rise is going to be.”

In the latest episode, there has been dramatically more central bank gold expended. Credible estimates suggest that more than 15,000 tonnes, or roughly half of the central banks’ supposed reserves, have already hit the market and are long gone, dangling from the wrists and necks of Indian women, filling vaults in the Middle East and Russia, and, in ever-greater quantity, migrating to China.

In the era of the London Gold Pool, only around 3,000 tonnes were sold to maintain the $35 price. This time the exercise has been dramatically larger and has occurred over a much longer time frame against the backdrop of a considerably more fragile financial structure, particularly in the West. So all of you are free to use your imagination to estimate how high gold is going to go this time.

It is critical to understand what the central banks have done because, in the absence of that knowledge, one cannot appreciate the whole gold story and will find it extremely difficult to recognise the investment opportunity being presented.

However, that is only one critical factor, and, as I said at the outset of my remarks, it is gold’s return as money that is going to be really instrumental in driving gold to prices that would seem fanciful to most at the present time. In reality, it isn’t gold that is changing, because it has been a constant store of value for 6,000 years. It is the value of fiat paper money in which gold is priced that is on the slippery slope to oblivion.

I could talk extensively about what is happening to the value of paper money, but to shorten things up, there is only one expression that you have to know: “quantitative easing.” What a joke that is!

The authorities would have you believe it is some sort of magic elixir and a panacea, but all it represents is the monetization of various forms of debt by unfettered printing of money by central banks. Because the inflationary impact has yet to occur, the linear thinkers would assure you that it isn’t going to be a problem. However, because of ongoing deleveraging and falling velocity of money in the short term, it is only being delayed.

As sure as death and taxes, continuing excessive money creation by the central banks will lead to accelerating inflation. When it begins to manifest itself, the velocity of money will pick up rapidly as people around the world rush to get rid of their increasingly worthless paper currency. In that event, we will rapidly progress from relatively benign inflation to truly frightening levels in a fairly short time.

At this point, I would like to repeat a quotation I used in a recent Investor’s Digest article. It comes from Ludwig Von Mises, the brilliant originator of the Austrian school of economics, which is the only formal economics that makes much sense to me. Long before I was born, which was a long time ago, Von Mises observed:

“There is no means of avoiding a final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner, as the result of a voluntary abandonment of further credit expansion, or later, as a final and total catastrophe of the currency system.”

That comment is pretty germane to what is unfolding today. Following what was arguably the most abusive credit cycle in history, Fed Chairman Ben Bernanke and his central banking confreres have clearly chosen the latter option, and accordingly, in my opinion, all forms of fiat paper money are headed for a train wreck. Ironically, Bernanke tipped his hand seven years ago in the infamous speech he gave before becoming Fed chairman. He claimed that he could combat deflation by the use of a printing press or, if need be, by dropping money from helicopters to sustain demand. To me his theories were ludicrous at that point and remain so today. Yes, he may avert deflation for a considerable time but at the very probable cost of hyperinflation and the social chaos that inevitably results.

Today the only question in my mind is whether investment demand for gold is going to go berserk as the result of a U.S. dollar collapse or because all the fiat currencies go down the drain together. The U.S. dollar is in its death throes, but will other countries print massive quantities of their own currencies to buy the dollar in an attempt to depress their currencies and keep their economies relatively competitive? To date, I would say that despite the considerable weakness in the dollar, there is abundant evidence that many other countries are printing aggressively to prevent their currencies from rising too much against the dollar.

In any case, I believe we are fated to see a continuing policy of ridiculous monetary ease around the globe, despite rhetoric to the contrary. This will occur because the idea of a double-dip recession or depression, as the case may be, is anathema to the powers that be. Very simply, withdrawing any significant amount of stimulus, be it monetary or fiscal, in the foreseeable future would virtually guarantee another deflationary event, and this time it may be impossible to stop.

Clearly, the United States is the lynchpin of the whole debacle, but most other countries are up their necks in the mess as well.

To begin, let us consider the United States’ fiscal quandary, with a federal government deficit currently running above 10 percent of gross domestic product and representing roughly 40 percent of government expenditures. These numbers are horrific for a country that is providing the world’s reserve currency. A recent study looked at the 28 examples of hyperinflation in various countries since 1980 and included Argentina, Zimbabwe, and many other banana republics. It noted that one common trait was that when the national government deficit exceeded 40 percent of expenditures, the point of no return had been reached. The U.S. is there as we speak and the $389 billion deficit in the first quarter of the 2010 fiscal year was far from reassuring.

While the preceding information is historical and thus factual, there is the matter of the Obama administration having recently admitted that its budget deficits would total $9 trillion (a number that I believe to be wildly optimistic) over the next 10 years. The question that obviously has to be asked is: What person, institution, or government, for that matter, in its right mind would lend money to the United States for the pathetically low interest rates currently on offer?

In reality, who would really be comfortable lending the United States money at any interest rate in the current circumstances, considering that higher rates would just ensure even higher deficits?

So it seems reasonable to assume that more of the deficits will have to be monetized, the dollar will inexorably decline as a result, and the question of confidence will become paramount. If confidence in the dollar is lost, chaos will ensue and those trapped in dollar-based fixed-income assets will see their wealth destroyed, the same fate that befell those who believed in the system in the Weimar inflation in Germany after World War I.

But the United States is far from the only country that is in serious difficulty. Things are as bad, and in certain cases worse, in many other countries. For example, Great Britain is a basket case, which incidentally looks real good on that hypocritical jerk Gordon Brown, who has led his country to ruin. Britain’s central bank has been forced to intensify its quantitative easing program several times to keep the economy barely afloat and its financial system semi-intact.

Japan, with its rapidly aging population, has seen its accumulated public debt reach 200 percent of GDP with no end of that trend in sight.

Europe is no bed of roses either. Despite the soothing words of the head of the European Central Bank, Jean Trichet, and some very vocal comments about current monetary excess from Germany’s Angela Merkel, they appear to have little choice but to keep the money flowing to save Club Med, Ireland, and a whole swath of eastern Europe from oblivion.

China, that paragon of all things economic and financial, had to resort to mandating a humongous increase in bank lending in the first half of last year to keep its economy moving. The ultimate outcome of this endeavor remains to be seen, although it certainly had a salutary impact on Chinese share prices and world commodity quotes. Unfortunately, the resulting massive over-capacity throughout the entire Chinese economy may become an issue.

That brings us to the favorite country of everyone in this room, Canada. I suspect that the Canadian authorities will be forced to deal with reality soon. Despite the hedge funds’ love affair with the Canadian dollar, the economic and financial fundamentals in this country don’t support the current level of the loonie. We are attached at the hip economically to the United States and as our dollar rises, our manufacturing industries or what’s left of them are being destroyed. Budget deficits are exploding at all levels of government.

One year ago the feds didn’t have one, but now the deficit is annualizing somewhere north of $60 billion. Ontario is homing in on $25 billion and even hydrocarbon power Alberta has ruefully admitted that its deficit forecast has risen to $6.9 billion, as very low natural gas prices, among other things, take their toll.

Bank of Canada head Mark Carney and Finance Minister Jim Flaherty know these problems all too well, although much of the public seems blithely unaware, and I am eagerly awaiting Carney and Flaherty’s response. Rumors of aggressive quantitative easing are growing, adding yet another nation to the expanding list practicing this dark art.

Why is all of this significant?

Very simply, it ensures that the demand side of the gold-silver equation is baked in the cake. Investment demand is exploding on a worldwide basis as those with wealth to protect are beginning to comprehend the true extent of the monetary debasement under way. This is only going to intensify as inflation begins to rear its ugly head as the result of the money-printing orgy.

As I mentioned earlier, the velocity of money is going to accelerate as people figure out what is occurring. Why would anyone want to hold a rapidly depreciating monetary asset when it yields next to nothing? At that juncture we will see if the powers that be have the courage to remove significant amounts of stimulus. Since I believe that our debt-logged economies will remain relatively weak and our financial structure exceedingly fragile, I don’t believe they will.

So I find it laughable when people concern themselves with reduced jewellery demand as a factor in the pricing of gold in the current circumstances. Any decline is being dramatically exceeded by rising investment demand, and this phenomenon is only going to intensify. Besides, all great bull markets in precious metals are driven by investment demand as gold reasserts itself in its true role as money. They most certainly don’t occur as the result of gold’s attraction a bauble or as an adornment.

However, as bullish as I am on the demand side of the equation, an equally compelling case can be made on the supply side, which consists of three primary elements — mine supply, scrap recovery, and central bank dispositions. The least important is scrap recovery, but it was briefly a negative in early 2009, when a lot of people around the world couldn’t wait to get rid of their jewelry and realize a little cash for the gold contained in it. However, that sharply abated in the second half of the year and the focus is now back where it should be, on mine supply and central bank dispositions.

One of the key factors that is going to contribute to the ongoing bull market is mine supply, or more accurately stated, lack thereof. Mine supply has been in a steady decline since early in the new century despite the constant rosy predictions of greater supply from the alleged industry expert GFMS Ltd. I have long been of the mind that the decline will continue for some time irrespective of what the gold price does. I base my opinion on numerous factors, including a dearth of quality projects ready for mining, continuing geopolitical and environmental issues, less high-grading as the gold price rises, ongoing capital constraints, and a chronic shortage of skilled miners and mine builders.

Thus I was fascinated when Aaron Regent, the new head of the world’s largest gold company, Barrick Gold, was quoted at RBC’s annual gold conference in London lamenting the state of the gold mining business. He went so far as to suggest that global gold production was in terminal decline despite record prices and Herculean efforts by mining companies to discover new orebodies in remote areas. He alluded to “peak gold,” implying that production has reached levels that can’t be exceeded, an expression that is commonplace in the oil industry, where the subject has been under discussion for some time.

Following this pessimistic assessment, a more horrifying prediction was revealed in the South African Journal of Science. Chris Hartnady, the research and technical director of a Cape Town based consultancy, stated that South Africa’s famous and extremely prolific Witwatersrand gold fields are around 95 percent exhausted and predicted that production rates should fall permanently below 100 tonnes per year within the next 10 years.

This is truly shocking in that gold production from the Witwatersrand, the largest gold field ever discovered, peaked at around 1,000 tonnes per annum in 1970 and, though falling steadily since, still contributes around 230 tonnes per year or roughly 10 percent of world production.

In view of these two evaluations by knowledgeable industry players, my negative view on production has been reinforced. Gold mine production is in the neighborhood of 2,350 tonnes per year, and I continue to believe that odds strongly favor it continuing to fall rather than show any meaningful increase for the next several years.

That brings me back to the central banks, and I apologize if I am belaboring the point, but I believe their role in the whole saga is neither widely appreciated nor well understood. Because of the remarkable obfuscation in the area, most observers do not realize how much central bank gold has entered the market in the past 15 years to fill the huge and growing gap between true demand and mine and scrap supply.

This is the direct result of misleading accounting by the central banks — accounting, incidentally, that has been endorsed by the International Monetary Fund, the very same IMF that has been threatening the gold market with potential massive sales for a number of years. The central banks have been permitted to use a one-line entry on their balance sheets, which does not differentiate between gold in the vault and gold receivables.

There is copious evidence, if you look for it, that supports the contention that gold receivables have grown dramatically as the result of central banks surreptitiously mobilizing their gold through leasing and swaps. This gold has been dumped in the market and has been essential in filling the natural demand- supply gap, which has probably exceeded 1,000 tonnes per year in most of the years since the mid- to late 1990s. That it also served to significantly depress the price wasn’t an accident.

The significance of the 1,000-tonne-per-annum number is two-fold. First, it represents in the neighborhood of 25 percent of the physical gold supply during the period, showing how truly deficient real sustainable supply is. Second, it virtually guarantees that Western central banks are getting dangerously short of reserves to continue this activity. Just as importantly a number of Eastern central banks — including China and Russia, to name but two — have acknowledged their intentions and are accumulating and will continue to accumulate gold as one avenue to diversify their reserves away from the U.S. dollar.

But India may have stolen a march on all of them when it announced recently that it had purchased 200 tonnes of the well-advertised and long-awaited IMF sale. This was the event that really kicked off the latest leg in the gold bull market, and unquestionably the Indian move drew widespread attention to a historic shift in the attitudes of central banks toward gold. It coincided with a complete cessation of selling by the European central banks, which under the terms of the recently renewed European Central Bank Gold Agreement could sell up to 400 tonnes per year.

Thus just as the Western central banks are being forced to wind down their incessant selling and leasing, the Asians have stepped up as buyers. This is a truly dramatic development and is going to have extremely positive ramifications for the gold price.

In view of the foregoing powerful positive fundamentals for the gold price, I find it almost nauseating that various pundits are referring to gold as overpriced and in a bubble phase. Nothing could be further from the truth, and, in reality, gold continues in its stealth bull market, which has now seen nine consecutive higher year-end closes. Despite this, as I mentioned earlier, it has attracted very little attention from the investing public in general.

The dedicated goldphile has participated throughout, and a number of sophisticated financial players have come on board recently, the latest being the legendary trader Paul Tudor Jones. But the average investor remains uninterested. It is instructive to remember that at the end of the last bull market in 1980, people were lined up around the block outside the Bank of Nova Scotia in downtown Toronto to purchase physical gold. Today the only lines that have formed are outside emporiums set up so the unsuspecting public can unload their gold jewelry for cash. To have a bubble of any significance, there has to be wide public belief, and it certainly isn’t on display in the gold market.

More importantly, if gold were overpriced, the gold producers would be experiencing an earnings bonanza. A close examination of the recent earnings statements of most major gold companies reveals that they are earning very little and are certainly not achieving the return on capital necessary to justify their involvement in a very risky and difficult business.

I find sentiment in the sector to be remarkably subdued in the face of compelling fundamentals. Many attractive junior gold stocks are not even keeping up with the rise in the gold price. If history were any guide, these stocks would be rising at three to four times the rate of the gain in the gold price, but investor skepticism is holding them back.

From a media perspective, if we were approaching the end of a bull market, the newspaper articles and television clips would be universally bullish touting the obvious merits of the yellow metal. There is indeed more coverage recently because of the relentless price rise, but it tends to be skeptical with the bearish commentators continuing to get the most exposure despite having been continuously wrong.

There is no better example of this than an individual who my compliance department would prefer that I not identify. However, I’ll give you a broad hint — he writes virtually daily for a noted Canadian gold Internet site. Dubbed the Tokyo Rose of gold commentators, he is always quoted in articles with a negative slant despite having been consistently wrong since the inception of gold’s bull market. In my opinion, as long as he gets any press at all, we are a long way from the end of this bull market in gold.

Finally, it is widely acknowledged that if the peak gold price in the last great bull market ($850 in January 1980) were to be adjusted to reflect the U.S. inflation rate in the intervening period, it would be equivalent to $2,300 today. That the current gold price is approximately half of that should put to rest any suggestion that this is a bubble.

That’s not to say there aren’t several bubbles forming in other financial markets (most notably in government debt instruments) as a result of a new bout of central bank madness, but gold is not on the list. In fact, I believe that we are many years and several thousands of dollars in price away from the end of this powerful bull market.

In conclusion, I now firmly believe that the chances of gold ever trading below $1,000 per ounce are remote. The only caveat I would offer is that if the world suffered a catastrophic deflationary collapse, an outcome long predicted by the noted Elliot Wave theorist Robert Prechter, gold could briefly be swept under but would then re-emerge with even greater relative strength as the only true safe haven. However, in a world of pure fiat currency, I think that a near-term deflationary outcome is highly unlikely. In fact, I strongly suspect that gold is going to stage a parabolic rise from current levels in the not-too-distant future, a development that will come as a shock to the many detractors of the world’s only real money.

Gold is the only real money because it isn’t someone else’s liability.

This remains one of the best supply-demand imbalance stories I have encountered in my long career and it will only be enhanced by the existence of massive short positions that will be impossible to cover amid myriad paper claims on gold that dwarf the physical supply, which, by the way, is a subject for another day.

Thanks very much for listening. It has been an honor to speak to you.

{kind=link}