By Eric Rosenbaum 01/26/10 – 12:06 PM EST

OMAHA, Neb. (TheStreet) — With Warren Buffett about as close as a capitalist can come to being canonized by the markets, Berkshire Hathaway(BRK.B Quote) can’t exactly fly under the radar. Still, one of the most unique aspects of Berkshire Hathaway is that, unlike other marquee securities within the U.S. corporate elite, Berkshire Hathaway’s shares have always traded on the QT.

This, of course, all changed last week, when Berkshire Hathaway’s B shares completed a 50-to-1 stock split.

Granted, five days of trading history with the new Berkshire B shares doesn’t provide much of a window onto long-term return potential. Average daily trading volume in the Berkshire Hathaway B shares has soared though, from 41,000 shares traded to as high as 6.6 million shares traded — and that was just on Monday. In the past five days, approximately 50 million Berkshire Hathaway shares have been traded.

Consider this: the 50 million Berkshire Hathaway shares traded over the past five days represent what would have previously amounted to almost three-and-a-half years’ worth of trading volume for the Berkshire Hathaway B shares.

It’s not hard to understand why there was such interest in Berkshire Hathaway after the stock split. The difference between a $3,400 share and a $70 share means the market’s most revered investment company can be purchased for a similar price to a few mail-order grass-fed Omaha steaks.

All of which justifies, by our way of thinking, a closer look at today’s new Buffett B shares. For that, read on….

Investors clearly feasted during the first days of the “Buffett for All” era; tt was a market-specific turn on a U.S.-specific cultural phenomenon. And it makes sense: this country has always been about transforming luxury into an item of mass consumption — the proverbial keeping up with the Jones’ — and, suddenly, Americans could keep up with the formerly off-limits stock of Warren Buffett.

Still, it would be wrong to get caught up in the publicity of the Berkshire Hathaway stock split as a reason, in and of itself, to purchase shares. Market analysts, and even Buffett himself, have shied away from placing too much emphasis on the historic event, and with good reason: intrinsic value doesn’t change just because one share becomes 50.

The critical question for investors then, amidst the stock-split publicity, is whether now is a uniquely good time to invest in the cut-rate version of Warren Buffett?

Ultimately, this question should lead investors to take two issues into consideration: what makes Berkshire Hathaway unique when its trading profile is no longer unique; and how Berkshire’s Hathaway’s underlying portfolio holdings are positioned given the economic outlook.

When it comes to stock structure, Berkshire Hathaway is a best-in-class stock that is effectively its own peer group. Standard & Poor’s classifies Berkshire Hathaway as a financial company, but that is really for lack of a definition that fits. And even though there are market conglomerates that seem hard to classify — such as a General Electric(GE Quote) making kitchen appliances and wind turbines, while also structuring mortgage pools and creating television programming — Berkshire’s unique three-pronged structure is what ultimately distinguishes it from the broader equities universe.

Berkshire’s first business pillar is the portfolio of public traded securities, the big names: Coke(KO Quote), Kraft(KFT Quote), Wal-Mart(WMT Quote) and Wells Fargo(WFC Quote), to name a few.

The other pillars of the Berkshire business are much harder to value than the public securities, and they are what make Berkshire a unique stock. If Berkshire were no more than a collection of big-cap U.S. companies, Buffett would likely be a little known mutual fund manager fighting the Sissyphean battle to beat the index returns year after year.

Insurance operations are the second big pillar of the Berkshire business, and as we have seen in the past two weeks, will continue to be a major driver for Berkshire shareholders. Berkshire Hathaway announced last week that it bought the biggest book of insurance business ever, from Swiss Re, for $1.3 billion. What’s more, Reuters reported on Tuesday morning that Berkshire has also increased its stake in Munich Re to $1 billion, or a 3% stake in the world’s biggest reinsurer.

Larry Coates, manager of the Oak Value Fund, which has Berkshire Hathaway as its largest holding, says the insurance business is ultimately a spread opportunity. The spread exists between the cost of underwriting insurance at a low cost of capital — with the Swiss Re transaction, Buffet estimates $50 billion in premium income over the next several decades — and being able to reinvest those profits. This spread has always been one of the key drivers of return for Berkshire.

Oak Capital Management’s Coates estimates that the Berkshire spread opportunity is between 50 to 150 basis points. For example, if Berkshire has 100 basis points in underwriting profits and can reinvest those profits at a 6% rate of return, it results in a 700 basis point spread.

“We’ve done analysis that shows that every 100 basis point change in the spread incrementally increase the value of Berkshire’s A share by $10,000,” Coates said.

The final pillar of the Berkshire portfolio is its wholly owned operating subsidiaries, among which Burlington Northern (BNI Quote) is about to become the newest addition.

These Berkshire Hathaway operating subsidiaries run the gamut across stocks tied very tightly to Buffett’s “all-in wager” on the U.S. economy. Housing, through Clayton Homes, and related stocks in the home furniture and carpet business, such as Shaw Industries.

This portion of the Berkshire portfolio is the one most sensitive to the cyclical nature of the economy. In addition to the focus on the housing market, Berkshire owns several jewelry companies. Anyone who has wandered into a Tiffany’s in the past few years and watched the flocks of salespeople descending on one customer buying a gold pen knows how sensitive these stocks are to economic peaks and valleys.

Thus, the cyclical stocks in the Berkshire Hathaway portfolio are a good place to look at what the company’s biggest backers think is its most unique trait in the current market: its undervaluation.

Granted, when it comes to discussing the Oracle of Omaha, Berkshire Hathaway shareholders often seem about as independently minded as the proverbial Jonestown Kool-Aid drinkers, but these days they are talking about some hefty discounts built into Berkshire shares as a result of its recent underperformance. It is not uncommon for long-time private investors to estimate the current Berkshire Hathaway valuation as 30%-35% below fair value. Buffett himself said last week on television that he thought the shares were the cheapest they had ever been, on a price-to-book ratio.

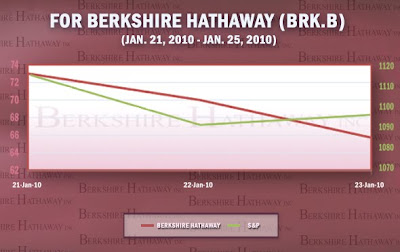

“There is more potential recovery in those operating subsidiaries than the market currently thinks,” said Bill Bergman, an analyst at Morningstar. Bergman believes fair value on Berkshire Hathaway’s B shares is $88 — the shares were at $68.84 at the close on Monday.

Jerome Bruni, a longtime private investor in Berkshire, says that Berkshire is selling at about 10x economic earnings, and for a company with its strength and outlook, that is cheap. He thinks that a conservative estimate values Berkshire Hathaway shares at least 25% higher.

Paul Lountzis, of Lountzis Asset Management, another longtime private investor in Berkshire, says the discount is 30% to 35% now.

Oak Value Fund’s Coates, who doesn’t make such bold claims, still said, “You can certainly say that Berkshire is undervalued by 30% or 40%. That undervaluation adds an attractive margin of safety at this point in the market cycle.”

Still, there are several reasons to believe that the hefty claims about Berkshire’s current undervaluation are not just the delirium of the Berkshire Kool-Aid drinkers.

Coates explained that the best time to buy cyclical companies is not going into a recession, but coming out of one. Over the next three to five years, Coates sees those operating subsidiaries in the niches of the housing market and the U.S. consumer market, more generally, as regaining their normalized earnings power. “Berkshire subsidiaries are far from a price-to-earnings peak right now,” Coates said.

Conventional market wisdom dictates that the biggest-cap names are usually the slowest to regain footing in a recovering economy.

This market dynamic played out last year, as the most beaten down, smaller-cap names recovered by wide margins. In the case of Berkshire’s public securities portfolio, this market dynamic suggests that Berkshire’s underperformance of the broad markets in 2009 may just mean its public securities are more attractively valued in a later stage of the economic recovery.

Morningstar’s Bergman noted that it is possible to construct many 12-month intervals during the past 15 years when the S&P 500 outperformed Berkshire shares.

What’s more, in each annual interval, the S&P 500 has outperformed Berkshire a third of the time. However, over the past 15 years Berkshire Hathaway shares have outperformed the S&P by a factor of two times.

“If we had $20 million in new money coming through the door in the next 90 days, based on where the Berkshire stock is trading now, there is a pretty good likelihood we would buy more,” Oak Value Fund’s Coates said.

The recent stock split may not matter in what makes Berkshire Hathaway unique as a security. It also doesn’t impact the argument as to whether Berkshire Hathaway is presently positioned as one of the market’s most attractively valued equities. However, Coates does think that all the talk about the S&P 500 adding Berkshire will prove correct. And if that happens, the most important repercussion won’t be all the index funds buying Berkshire, but that Berkshire will suddenly become a big factor in investor benchmarking.

“If you don’t invest in Berkshire, you will effectively be shorting the company, making a bet against Buffett,” Coates argues.

As a result, there is likely to be much greater research coverage of Berkshire Hathaway. “Berkshire is a company where if you go to a cocktail party, everyone has an opinion, but a very small number of them are qualified to have one. If the byproduct of the stock split is that it eliminates the disincentive that exists for research coverage, then maybe it does benefit us, perhaps leading to a reduction in the current discount,” Coates said.

Courtesy of the Berkshire Hathaway stock split, the party invite list just got a lot bigger. And if you believe the Berkshire bulls, it’s time to RSVP: there is still, it seems, a long way to go before the current discount in Berkshire Hathaway shares is eliminated.

— Reported by Eric Rosenbaum in New York.

Share Investor Links

Share Investor Blog – Stockmarket & Business commentary

Share Investor New Zealand Business News– Get more business news

Discuss this topic @ Share Investor Forum – Register free

Share Investor’s Daily Forex Updates

Recommended Amazon Reading

WFC 4Q09_Review

WFC 4Q09_Review